Featured

Table of Contents

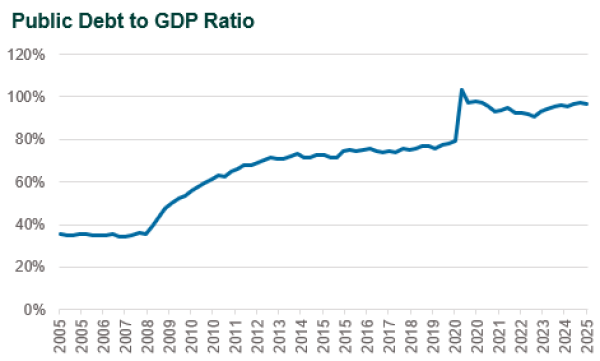

Total insolvency filings increased 11 percent, with increases in both company and non-business insolvencies, in the twelve-month period ending Dec. 31, 2025. According to stats launched by the Administrative Workplace of the U.S. Courts, annual personal bankruptcy filings totaled 574,314 in the year ending December 2025, compared to 517,308 cases in the previous year.

Non-business bankruptcy filings increased 11.2 percent to 549,577, compared with 494,201 in December 2024. Personal bankruptcy totals for the previous 12 months are reported 4 times every year.

For more on bankruptcy and its chapters, view the list below resources:.

As we get in 2026, the insolvency landscape is anticipated to move in methods that will considerably impact financial institutions this year. After years of post-pandemic uncertainty, filings are climbing steadily, and financial pressures continue to impact consumer habits.

Official State Programs for Debt Relief

The most popular trend for 2026 is a continual boost in personal bankruptcy filings. While filings have not reached pre-COVID levels, month-over-month development recommends we're on track to surpass them quickly.

While chapter 13 filings continue to increase, chapter 7 filings, the most typical type of consumer bankruptcy, are anticipated to dominate court dockets. This trend is driven by customers' lack of disposable income and installing financial stress. Other crucial motorists include: Consistent inflation and elevated rate of interest Record-high credit card debt and diminished cost savings Resumption of federal trainee loan payments Regardless of recent rate cuts by the Federal Reserve, rate of interest remain high, and borrowing expenses continue to climb.

Indicators such as consumers using "buy now, pay later" for groceries and surrendering recently bought cars show monetary tension. As a financial institution, you may see more foreclosures and lorry surrenders in the coming months and year. You should likewise get ready for increased delinquency rates on vehicle loans and home mortgages. It's also essential to carefully keep an eye on credit portfolios as financial obligation levels stay high.

We forecast that the genuine impact will strike in 2027, when these foreclosures move to completion and trigger insolvency filings. How can lenders stay one action ahead of mortgage-related bankruptcy filings?

New Rules for Filing Bankruptcy in 2026

Many approaching defaults may arise from previously strong credit sectors. In the last few years, credit reporting in bankruptcy cases has actually ended up being one of the most contentious subjects. This year will be no different. But it's essential that lenders stand company. If a debtor does not declare a loan, you ought to not continue reporting the account as active.

Resume typical reporting just after a reaffirmation agreement is signed and filed. For Chapter 13 cases, follow the plan terms thoroughly and consult compliance teams on reporting commitments.

These cases typically create procedural complications for financial institutions. Some debtors may fail to properly reveal their possessions, income and expenditures. Again, these issues add intricacy to personal bankruptcy cases.

Some recent college graduates might manage responsibilities and turn to insolvency to manage overall debt. The takeaway: Creditors must prepare for more complex case management and consider proactive outreach to borrowers facing considerable monetary strain. Lastly, lien perfection remains a major compliance danger. The failure to best a lien within 1 month of loan origination can lead to a lender being dealt with as unsecured in insolvency.

Consider protective steps such as UCC filings when hold-ups occur. The insolvency landscape in 2026 will continue to be shaped by financial uncertainty, regulatory analysis and developing customer behavior.

Negotiating Your Total Debt With Professional Services

By expecting the patterns mentioned above, you can mitigate exposure and maintain operational strength in the year ahead. This blog site is not a solicitation for organization, and it is not intended to make up legal recommendations on particular matters, create an attorney-client relationship or be lawfully binding in any method.

With a quarter of this century behind us, we go into 2026 with hope and optimism for the brand-new year. Nevertheless, there are a variety of concerns many merchants are coming to grips with, including a high financial obligation load, how to use AI, diminish, inflationary pressures, tariffs and waning need as price continues.

Protecting Your Financial Rights Against Debt HarassmentReuters reports that luxury merchant Saks Global is preparing to apply for an imminent Chapter 11 personal bankruptcy. According to Bloomberg, the business is talking about a $1.25 billion debtor-in-possession funding package with financial institutions. The company sadly is encumbered substantial financial obligation from its merger with Neiman Marcus in 2024. Added to this is the basic global downturn in high-end sales, which might be essential aspects for a possible Chapter 11 filing.

Protecting Your Financial Rights Against Debt Harassment17, 2025. Yahoo Finance reports GameStop's core business continues to battle. The company's $821 million in net revenue was down 4.5% year-over-year, driven by a 12% decline in hardware and a 27% decline in software application sales. According to Seeking Alpha, a key component the company's relentless earnings decrease and lessened sales was last year's unfavorable weather conditions.

Benefits and Cons of Debt Settlement in 2026

Pool Magazine reports the business's 1-to-20 reverse stock split in the Fall of 2025 was both to guarantee the Nasdaq's minimum bid cost requirement to preserve the company's listing and let investors understand management was taking active measures to resolve financial standing. It is unclear whether these efforts by management and a much better weather climate for 2026 will help avoid a restructuring.

, the chances of distress is over 50%.

{kind=link}

Latest Posts

Managing Your Credit Future After Insolvency

Know Your Protected Rights Against Aggressive Collectors

Free Credit Counseling Benefits in 2026